TLDR

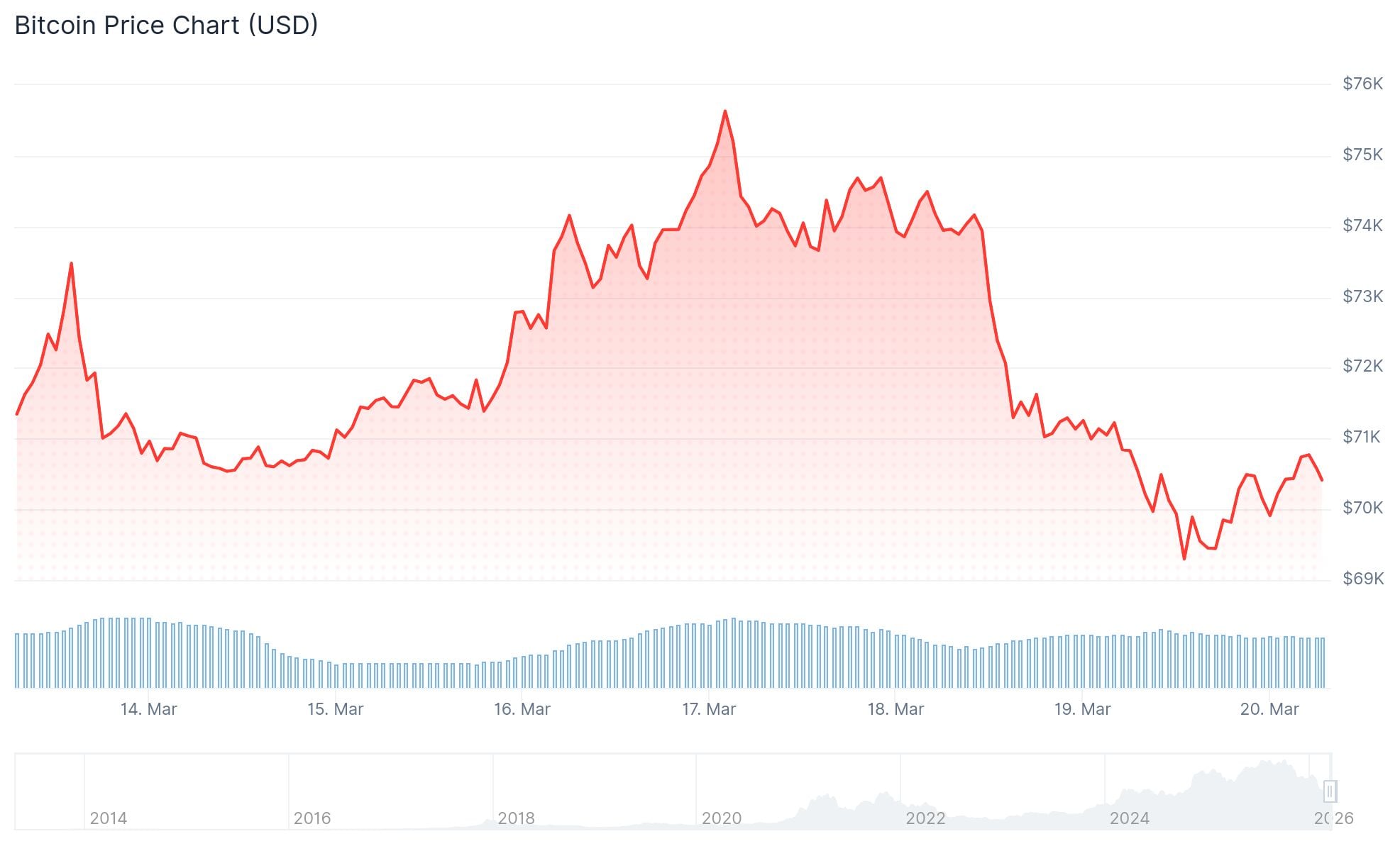

- Bitcoin jumped to $70,800, up over 1%, after major economies announced steps to stabilize energy markets and reopen the Strait of Hormuz.

- Oil prices fell nearly 2%, with WTI crude dropping to $93.80 after Britain, France, Germany, Italy, the Netherlands, and Japan issued a joint statement.

- Ether, XRP, and Solana saw smaller gains of less than 1%, lagging behind Bitcoin.

- The S&P 500 closed below its 200-day moving average for the first time since May last year, signaling a bearish shift.

- The Federal Reserve has signaled rates are likely to stay put, with markets not expecting a cut despite one remaining on the table.

Bitcoin led a broad crypto market recovery on Friday as falling oil prices gave risk assets some room to breathe. The world’s largest cryptocurrency climbed to $70,800, up more than 1% on the day, after dipping below $68,900 overnight.

The gains came as six major economies — Britain, France, Germany, Italy, the Netherlands, and Japan — issued a joint statement condemning Iran’s attacks and pledging to help ensure safe passage through the Strait of Hormuz. The statement was released through UK Prime Minister Keir Starmer’s office.

West Texas Intermediate crude fell nearly 2% to $93.80 following the announcement. Brent crude saw similar losses. U.S. Treasury Secretary Scott Bessent had also said on Thursday that the U.S. may lift sanctions on Iranian oil tankers and could tap its Strategic Petroleum Reserve.

Other cryptocurrencies saw smaller moves. Ether, XRP, and Solana each gained less than 1%, trailing Bitcoin’s recovery.

Despite the bounce, uncertainty remains. The Middle East conflict is ongoing, and WTI crude continues to trade well above pre-war levels, holding near a key support level around $92. Analysts at Mott Capital Management said oil still has a higher bias while it holds that support.

Stocks Under Pressure

Stock markets remained under strain heading into the end of the week. U.S. index futures edged higher Friday morning, with Dow futures rising 0.2% and S&P 500 futures up 0.1%. But the broader trend remains negative.

Major U.S. indexes are on track for a fourth straight week of losses. The Dow is down around 1.2% for the week, while the S&P 500 is off about 0.4% and the Nasdaq is down roughly 0.1%. Both the Dow and Nasdaq are sitting around 8% below their recent record highs.

On Thursday, the S&P 500 closed below its 200-day simple moving average for the first time since May last year. That move is often watched by traders as a sign of a broader shift in market momentum.

https://twitter.com/TrendSpider/status/2034691377775145236?s=20

Sentiment got a small lift after Israeli Prime Minister Benjamin Netanyahu said Israel was supporting U.S. efforts through intelligence sharing and other channels aimed at reopening the Strait of Hormuz. He also suggested the conflict could end sooner than many fear.

Fed Stance Keeps Pressure On

The Federal Reserve this week signaled growing uncertainty over both growth and inflation. Fed Chair Jerome Powell’s comments left markets expecting rates to stay unchanged for now, even though officials said one cut could still happen this year.

That has left both crypto and traditional markets exposed to oil price moves, with little support from expected rate cuts.

On the corporate side, earnings season is largely over for the quarter. GameStop and Carnival are set to report results next week.

🚨 Our JUNE Stock Picks Are Live!

A new month means new opportunities. Our analysts have just released their top stock picks for June, highlighting companies with strong momentum that rank highly on our KO Score algorithm. We’re also now sharing trade ideas for both long-term and short-term investors, giving you more ways to spot potential opportunities in the market.

Sign up to Knockout Stocks today and get 50% off to unlock the full list and see which stocks made the cut.

Use coupon code Special50 for your exclusive discount!

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants