Stock: Q2 Revenue Beats but Shares Sink 7.7% on Profit Miss")

TLDRs:

- AWS Q2 revenue hits $30.87B, up 18%, slightly ahead of expectations.

- Operating income falls short at $10.2B vs. $10.9B expected, sparking selloff.

- AMZN shares drop 7.7% to $216.07 despite cloud division strength.

- AI-related investments and margin pressure weigh on Amazon’s future outlook.

Amazon Web Services (AWS) posted $30.87 billion in Q2 revenue, marking an 18% year-over-year increase and narrowly beating Wall Street expectations.

The robust revenue performance confirmed AWS’s ongoing dominance in the global cloud infrastructure market, where it continues to be a leader alongside Microsoft Azure and Google Cloud.

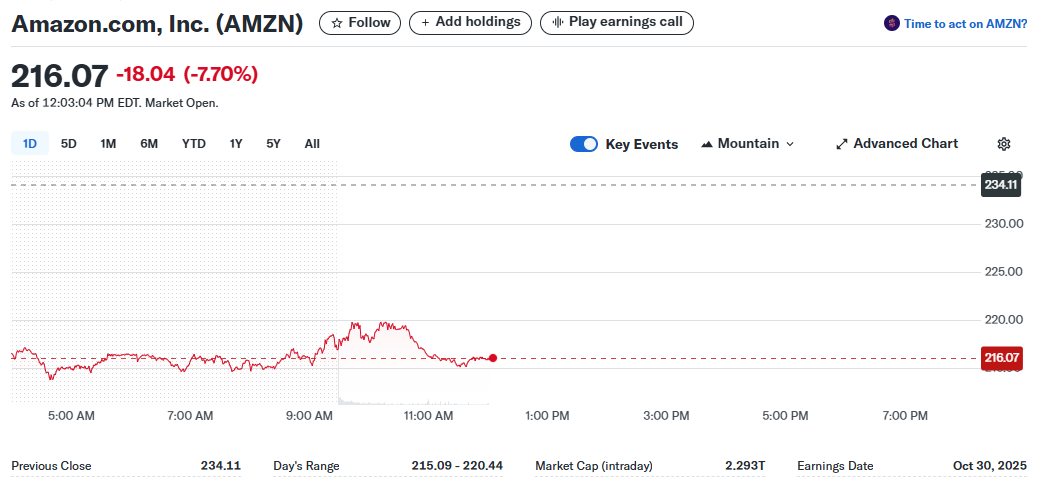

Despite the solid top-line numbers, Amazon’s cloud division generated $10.2 billion in operating income, below the $10.9 billion consensus forecast. The shortfall triggered a selloff, with Amazon.com, Inc. ($AMZN) stock plummeting 7.7% during Friday trading to $216.07, down from a previous close of $234.11.

The company’s Q2 results reflect an increasingly competitive landscape. While AWS maintains a strong revenue base, Microsoft and Google are growing at faster rates, 39% and 32%, respectively, fueled by enterprise AI adoption and aggressive infrastructure buildouts.

AI-Fueled Cloud Demand Can’t Offset Margin Concerns

AI remains a central growth driver in cloud infrastructure, benefiting all major providers. However, the capital-intensive nature of building and maintaining AI-ready data centers has begun to squeeze profit margins, particularly for AWS.

AWS’s operating margin dropped to 32.9% in Q2, down from 39.5% in the previous quarter. The decline is attributed to Amazon’s increased spending on infrastructure, specifically for AI workloads that require custom chips and specialized configurations.

CEO Andy Jassy has committed to ramping up investments in AI infrastructure, signaling that Amazon sees long-term opportunity in the space, even at the cost of short-term profit compression. The company also announced plans to open a new AWS region in Chile by 2027, highlighting its global expansion ambitions.

Stock Sinks Despite Guidance Above Street Forecast

Although Q2 revenue outpaced expectations, Amazon’s future guidance failed to fully reassure investors. The company expects Q3 operating income between $15.5 billion and $20.5 billion, with revenue projected between $174 billion and $179.5 billion.

While the sales outlook is slightly above analyst estimates, the midpoint of operating income guidance trails expectations.

The lukewarm profit forecast and the noticeable margin drop triggered concern over whether Amazon can balance AI investments with sustainable earnings growth. Investors appeared unimpressed by the better-than-expected revenue, focusing instead on shrinking margins and the uncertain payoff timeline of Amazon’s cloud infrastructure expansion.

Amazon’s Cloud Lead Faces a New Reality

While AWS still commands roughly one-third of the global cloud market, its lead is under threat. Analysts, including Gil Luria of D.A. Davidson, warn that Microsoft could overtake AWS as early as next year if current growth rates persist.

The scenario underscores a broader shift in tech, where market share dominance can erode rapidly under competitive pressure. As AI becomes the core battleground in cloud services, Amazon’s aggressive spending may be necessary to avoid obsolescence, but it comes at a steep financial cost.

For now, the market is signaling caution. Amazon stock, which had been up 6.7% year-to-date, saw a steep correction post-earnings, highlighting investor anxiety over how long it will take for AWS’s AI investments to translate into bottom-line growth.

Considering a new stock? You may want to see what’s on our watchlist first.

Our team at Knockout Stocks follows top-performing analysts and market-moving trends to spot potential winners early. We’ve identified five stocks gaining quiet attention that could be worth watching now. Create your free account to unlock the full report and get ongoing stock insights.Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants