MetaMask has 30 million users and now ships a Mastercard. Trust Wallet has 60 million users across 100+ chains. Phantom runs Phantom Cash on Solana rails. In 2026, every major wallet finally has a way to spend — and under the hood, most of them work the same way: stablecoin rails, Visa or Mastercard settlement, a card partner handling the balance. The question is no longer whether you can spend from self-custody. It is what the wallet layer is actually doing before your funds hit the card.

The card flows behind the MetaMask Card, Phantom Cash, and the Chimera Card all end up on stablecoin rails — that is how Visa and Mastercard work. What matters is everything that happens before that: how the wallet holds your Bitcoin, how it moves, what it costs to transact, what the platform does with your data, and who is incentivised by your usage. This comparison walks through each wallet honestly, then looks at where Chimera Wallet — the newest entrant, and the only one built on Arkade, a Bitcoin Layer 2 designed for true peer-to-peer transactions — actually differentiates. If you have been searching for a serious MetaMask alternative or Trust Wallet alternative with lower fees, better privacy, and a non-custodial architecture built around bitcoin self custody at the wallet layer, the shortlist has changed.

Quick Summary

- MetaMask (30M users) now supports native Bitcoin alongside Solana, Monad, and its historical EVM base. The MetaMask Card (Mastercard, via Baanx) launched February 2026, spending USDC, USDT, and WETH at any Mastercard terminal.

- Trust Wallet (60M users) supports native Bitcoin and 100+ chains as a mobile-first self-custody wallet. No standalone spending card.

- Phantom supports native Bitcoin (including Ordinals and BRC-20) alongside Solana and EVM. Phantom Cash launched late 2025 as a Visa card drawing from a Solana-secured Cash balance.

- Chimera Wallet is a non-custodial wallet built on Arkade — a Bitcoin Layer 2 designed for true peer-to-peer transactions with lower fees and stronger privacy than Lightning or L1. The Chimera Card (Visa, via Wirex Pay) is open for pre-order, available in 50+ countries. Card services and CEXT token issuance are handled by separate licensed partners; the wallet itself is developed by a Chimera Association.

- Chimera launched April 20, 2026 as a Progressive Web App (PWA) — browser-distributed, installable on any device, with no App Store dependency.

- Current PWA scope (v0.1): Bitcoin only, with multi-asset support (ETH, USDT, Tron, Polygon) and the CEXT token launching through the end of May 2026.

What the Wallet Actually Does

The biggest wallets in crypto spent 2024 and 2025 racing to close the spending gap — and they got there. MetaMask added a Mastercard in February 2026, Phantom shipped Phantom Cash late last year, Trust Wallet partners with several third-party card providers. Under the hood, all of these cards work the same way at the settlement layer: the wallet’s balance is converted to a stablecoin (USDT or USDC), the card transaction clears through Visa or Mastercard, and a card partner handles the float. The Chimera Card is the same — funds are topped up into USDT for settlement through Wirex Pay. This is how every Visa card in crypto works. There is no way around it, and pretending otherwise would be dishonest.

So the question for anyone thinking about switching in 2026 is not “whose card is different?” The cards are broadly similar. The real question is: what is the wallet layer actually doing? That is where the products genuinely diverge.

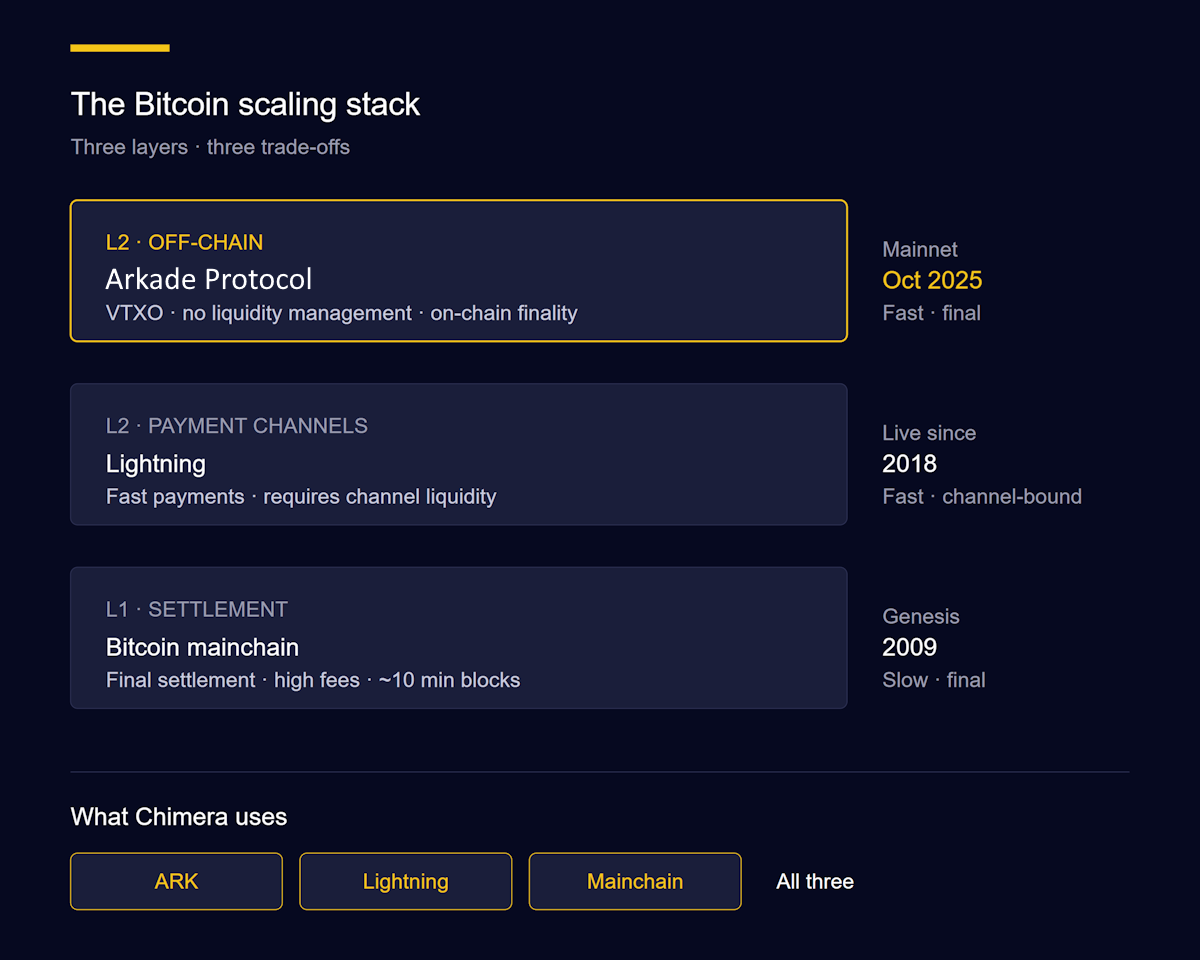

The MetaMask wallet is an extension-first product built around EVM DeFi, with Bitcoin added to the UI as a convenience layer. The Phantom wallet is Solana-first with Bitcoin and EVM bolted on. Trust Wallet is a breadth play — 100+ chains, one mobile app. Chimera is different at the wallet layer in three ways that affect day-to-day use: it runs on Arkade, a Bitcoin Layer 2 designed for true peer-to-peer transactions rather than channel-based routing (Lightning) or on-chain settlement (L1); it charges materially lower fees at the wallet level than any wallet settling on L1 Bitcoin or Lightning; and it operates under a non-profit software structure that changes the incentive around user data and monetisation.

For a user who transacts in Bitcoin regularly — moving funds between wallets, topping up a card, paying a counterparty — what happens inside the wallet determines the cost, speed, and privacy of every transaction. That is the gap Chimera is built to close. Not the existence of a card, which every major wallet now has. The wallet experience that sits behind it.

MetaMask Review

MetaMask in April 2026 is no longer just the EVM wallet — it supports native Bitcoin, Solana, and Monad, and it spends stablecoins at any Mastercard terminal through the MetaMask Card. But the wallet layer carries trade-offs that add up quickly in daily use.

With roughly 30 million monthly users, MetaMask is the most recognisable self-custody wallet in crypto. It earned that position through deep EVM integration, first-class DeFi support, and a browser extension that made Ethereum approachable for a generation of early users. The product has materially expanded since: native Bitcoin was added to the core UI in early 2026, Solana and Monad support followed, and the MetaMask Card (a February 2026 Mastercard collaboration with Baanx) lets users spend USDC, USDT, and WETH directly from self-custody. For active DeFi users, MetaMask is still the reference.

The trade-offs, however, are real — and concentrated in two places: the attack surface, and the cost of moving money.

The browser extension model is the single most-exploited surface in crypto. Fake plugins, cloned extensions, and poisoned dApp interactions have produced the majority of publicly reported Ethereum wallet compromises — fake signing prompts, malicious dApp approvals, and transaction spoofing are a constant tax that ConsenSys itself documents extensively. There is a reason the same attack patterns keep appearing in incident reports year after year: extensions run inside an environment with very little scrutiny or control, and users cannot easily tell a legitimate MetaMask plugin from a malicious clone.

Then there is the cost of actually using it. Spreads on MetaMask in-wallet swaps run materially above what users pay on comparable non-custodial alternatives — in practice, often 3× or more the equivalent fee on a wallet built around cleaner routing. On Bitcoin specifically, the story is worse: MetaMask’s Bitcoin support is L1-only, with no Lightning and no Arkade integration, so any Bitcoin transaction carries full mainchain fees and ~10-minute confirmation times. For a user moving Bitcoin regularly — topping up a card, paying a counterparty, rebalancing between wallets — that friction is not theoretical. It is a per-transaction tax paid on top of everything else.

Users searching for a MetaMask alternative in 2026 are usually not looking for a wallet that cannot do DeFi. They are looking for lower spreads, a cleaner attack surface, and a way to transact in Bitcoin without L1 fees on every move.

Best for: DeFi users, NFT traders, cross-chain active users, anyone whose activity centres on EVM and who is comfortable spending stablecoins.

Not for: users who want low-fee Bitcoin transactions, users uncomfortable with the browser-extension attack surface.

Trust Wallet Review

Trust Wallet is the widest-coverage self-custody wallet in the consumer market — 100+ chains, full native Bitcoin support, no standalone card, with App Store exposure that has repeatedly disrupted distribution.

Trust Wallet’s 60 million users are the largest installed base in self-custody crypto. The product’s core pitch has always been breadth, and it has delivered: full native Bitcoin (SegWit and legacy), Ethereum, Solana, BNB Chain, and over a hundred other networks, in a single mobile app. For users who want one wallet across the broadest possible set of chains, it is the reference choice.

The real trade-off for Trust Wallet is distributional rather than architectural. Like most consumer crypto wallets — Chimera included — Trust Wallet relies on third-party partners for fiat on-ramps, card-adjacent services, and certain swap flows. That is how regulated financial products work at consumer scale, and it is not unique to Trust Wallet. What is unique is how often Trust Wallet has been removed, restricted, or delisted from App Stores in various jurisdictions, with the pace accelerating after Google’s October 2025 policy update requiring custodial wallet features to hold active licences in every jurisdiction of operation. Users in affected regions have had to sideload, switch devices, or abandon the wallet entirely.

And unlike MetaMask or Phantom, Trust Wallet has no first-party spending card. Users who want checkout-level spending typically route through a third-party card product, with custody terms and fees that vary by region. This is the main reason searches for a Trust Wallet alternative have accelerated through early 2026.

Best for: multi-chain users, anyone who wants one mobile app across 100+ networks. Not for: users who want a first-party spending card, users in regions with App Store enforcement issues.

Phantom wallet Review

Phantom ships native Bitcoin, Ordinals, and BRC-20 support alongside its Solana and EVM foundation, and Phantom Cash provides a Visa card drawing from a Solana-secured balance.

Phantom earned its reputation the right way: by making Solana feel instant. The animations, the signing flow, the built-in swap interface — everything is tight. For the Solana ecosystem, nothing else comes close. Phantom added native Bitcoin support (including Ordinals and BRC-20) in late 2023, and the product is now a genuine multi-chain wallet covering SOL, EVM, and BTC.

Phantom Cash, launched late 2025, is a Visa card (virtual and physical) drawing from a Solana-secured Cash balance inside the Phantom app. It is a clean product. The architectural note for anyone comparing cards is that Phantom Cash routes through Solana before settlement: the Cash balance is Solana-denominated, so spending from any other asset — Bitcoin included — involves a conversion step into that balance first. This is not unique to Phantom; every major wallet’s card sits on top of a conversion layer of some kind (the Chimera Card top-up converts into USDT via Wirex Pay, for example). What differs is the layer the conversion happens on — Phantom’s is Solana, and that means users pay Solana network conditions and routing for every top-up.

Phantom’s Bitcoin support at the wallet level is native and well-executed, but it is L1-only — no Lightning integration, no Arkade, no L2 scaling. Bitcoin transactions inside the Phantom wallet carry mainchain fees and mainchain confirmation times. This is a perfectly reasonable choice for a wallet whose centre of gravity is Solana, but it is a material architectural difference from a wallet built around Bitcoin L2 infrastructure.

Best for: Solana-native users, cross-chain users who want one wallet for SOL, EVM, and BTC, anyone whose card usage is comfortable routing through a Solana Cash balance.

Not for: users who want low-fee Bitcoin transactions at the wallet layer, users who want Lightning or Arkade Bitcoin L2 support.

Chimera Wallet vs Competitors

Chimera Wallet is a non-custodial, open-source self-custody wallet built on Arkade — the new Bitcoin Layer 2 backed by Tether, Tim Draper, Anchorage Digital, and Ego Death Capital. It pairs a first-class Bitcoin experience with financial services delivered through third-party partners, and it is the only wallet in this comparison where the software layer is developed by a Chimera Association rather than a for-profit company.

Chimera takes a different architectural approach from the incumbents. The software — the wallet itself — is open-source and developed by a non-profit association. The services that wrap around the wallet (card issuance, fiat ramps, token infrastructure) are delivered by separate third-party partners: Wirex Pay handles the card rails, and other licensed partners handle the CEXT utility token and card-adjacent services. This separation is deliberate. It means the software layer has no fee-extraction mandate, while the financial services are handled by the companies legally structured to handle them. Independent coverage — including a detailed chimera wallet review published separately — has focused on this separation as the product’s defining architectural decision.

At the wallet level, Chimera is the first Bitcoin super-app to integrate Arkade as its primary payment layer with multi-asset support rolling out through May 2026. The Chimera Card is a Visa card powered by Wirex Pay: you top it up from the wallet, the top-up is converted to USDT in-app, and settlement happens through Wirex Pay on standard Visa rails. This is how every major crypto card works — MetaMask Card, Phantom Cash, and Chimera Card all route through stablecoin rails at settlement. The chimera wallet vs metamask question is not about the card, then, but about the wallet beneath it: MetaMask is an extension-first cross-chain wallet with an L1-only Bitcoin implementation; Chimera is a PWA-distributed wallet running all three Bitcoin layers (mainchain, Lightning, and Arkade) at lower fees and with stronger privacy. The chimera wallet vs trust wallet comparison is closer, and fairer: both are mobile-friendly self-custody wallets, but Chimera runs on a non-profit software structure and pairs it with genuinely decentralised Bitcoin infrastructure rather than breadth-over-depth chain coverage.

Arkade, and Who Chose It

The wallet is built on Arkade — a Bitcoin Layer 2 that uses VTXOs (Virtual UTXOs, short-lived off-chain Bitcoin commitments that settle on-chain when needed) to combine Lightning-level speed with mainchain-level finality. Arkade launched on mainnet in October 2025, backed by investors including Tether, Tim Draper, Anchorage Digital, and Ego Death Capital — investors who have spent years identifying what counts as real Bitcoin infrastructure. When that set of names converges on a new protocol, it carries weight that no marketing claim from a wallet ever could.

Chimera is built natively on Arkade – one of the most complete Bitcoin super-app to integrate Arkade as its primary payment layer rather than as an add-on.

Distribution

Chimera is distributed as a Progressive Web App — a browser-based application that installs to the home screen without going through an App Store. Google’s October 2025 policy update requires custodial wallet features to hold active licences in every jurisdiction they operate in, or face removal. By being PWA-only, Chimera stays accessible regardless of future App Store policy shifts — no platform-level decision can take it off a user’s device.

The Chimera Card

The Chimera Card is a Visa card powered by Wirex Pay, available in 50+ countries across Europe, Asia-Pacific, and Latin America. Top-ups are initiated in-app from the Chimera Wallet — the user selects a funding asset, the amount is converted to USDT inside the app, and the card is loaded through Wirex Pay for spending on the Visa network. Pre-orders are live now: 1,000 priority cards at a 20 CHF reservation fee, with virtual cards shipping first and physical cards following. Pre-order holders lock in 1.5% transaction fees (versus 2% standard) and 0% top-up fees (versus 1% standard) for the lifetime of the account. The card requires light KYC through the in-app flow.

The card itself is not the differentiator — every major wallet has a Visa or Mastercard product now, and they all settle through stablecoin rails because that is how card networks work. What is different is the wallet experience behind it: lower in-wallet swap spreads than any competitor in this comparison, Arkade-based Bitcoin transactions that settle in seconds for fractions of a cent, and a non-profit software layer with no incentive to extract value from users.

Feature Comparison

| Feature | MetaMask | Trust Wallet | Phantom | Chimera |

| Bitcoin wallet layer | L1 only (2026) | L1 (full, native) | L1, Ordinals, BRC-20 | L1 + Lightning + Arkade L2 |

| Chain coverage | BTC + EVM + SOL + Monad | 100+ chains | SOL + EVM + BTC | BTC today, multi-asset by end of May 2026 |

| First-party spending card | MetaMask Card (Mastercard) | None | Phantom Cash (Visa) | Chimera Card (Visa) |

| Card settlement rail | Stablecoin → Mastercard | — | Solana Cash balance → Visa | USDT → Visa (Wirex Pay) |

| Non-custodial keys | ✓ | ✓ | ✓ | ✓ |

| Primary distribution | Extension + mobile app | Mobile app | Mobile app | PWA |

| Software-layer structure | For-profit (ConsenSys) | For-profit (Binance-affiliated) | For-profit (Paradigm-led) | Chimera Association |

| Financial services provider | ConsenSys / Baanx | Third-party partners | Phantom | Wirex Pay, Switzerland-based regulated partners |

Scope note: at publication, the Chimera PWA (v0.1) supports Bitcoin only. Multi-asset support (ETH, USDT, Tron, Polygon) is scheduled for end of May 2026, alongside the CEXT token launch on May 20. Chimera is positioned as a direct alternative to Trust Wallet and Phantom for users who want genuinely decentralised self-custody with a non-profit software layer and lower fees, and as a Bitcoin-depth complement to MetaMask for users whose primary holdings are Bitcoin.

The Non-Profit Difference

Unlike all three competitors, Chimera Wallet is developed by the Chimera Association — with financial and commercial services delivered separately by third-party partners.

MetaMask is owned by ConsenSys. Trust Wallet is affiliated with Binance. Phantom raised institutional capital at a multi-billion valuation led by Paradigm. All three are for-profit businesses. That is not a criticism — it is a fact about their incentive structures. Every feature, every swap fee, every integration in those wallets ultimately serves a return expectation to equity holders.

Chimera’s architecture separates the software from the services. The wallet itself — the open-source code that holds user keys, signs transactions, and connects to Arkade — is developed by the Chimera Association and has no revenue-maximisation mandate. Services that sit alongside the wallet are delivered by separate third-party partners: Wirex Pay handles card issuance, other licensed partners operate token infrastructure and card-adjacent services, and additional partners cover fiat ramps and gift cards. The non-profit does not issue cards, does not hold user funds, does not take fees on third-party services. This is a common legal structure for European “sovereign tech” projects where the goal is long-term public infrastructure rather than equity returns.

This does not mean Chimera is a tokenless project — the CEXT utility token is a core part of the ecosystem, with fee discounts, referral multipliers, and governance mechanics for holders. The difference is structural: the token is issued by a separate licensed entity, the software that holds user keys is developed by the non-profit, and neither is dependent on the other to function. For users who have watched wallet products slowly drift into hidden swap spreads, sponsored placements, and promoted integrations that serve a return rather than the user, the separation of software from services is worth weighing when choosing among the best non-custodial wallets available in 2026.

Best Crypto Debit Cards 2026

Every Visa and Mastercard transaction clears on the card network in USD. The useful comparison for crypto cards in 2026 is not which card “spends Bitcoin” — it is what the wallet behind the card is doing before your funds reach the card network.

Most products marketed as a crypto debit card or bitcoin debit card in 2026 use the same core mechanics: the user converts a crypto balance into a stablecoin (or a cash balance), that balance is topped up onto a Visa or Mastercard, and the card settles every purchase in USD on the card network. This is how card networks work at scale — the rails are USD-denominated, and even self-custody wallet cards route through a top-up and conversion step before the transaction clears. The architectural differences between crypto cards therefore do not live at the card level. They live in the wallet.

So the real comparison is architectural. Where does the custody handoff happen? What does the wallet layer look like before the card transaction starts? What does the user pay in fees along the way, and what does the platform do with their data?

| Card | Wallet layer | Top-up asset (in app) | Settlement rail | Coverage | Issuing partner |

| Chimera Card | Non-custodial PWA, Arkade L2 Bitcoin support | USDT (converted in-app) | Visa · USD | 50+ countries | Wirex Pay |

| MetaMask Card | Browser extension + mobile, L1 Bitcoin | USDC · USDT · WETH (direct) | Mastercard · USD | Mastercard network | Baanx |

| Phantom Cash | Mobile wallet, Solana-first | Cash balance (Solana-secured) | Visa · USD | Visa network | Phantom |

| Exchange cards (Coinbase, Binance) | Custodial account | Exchange balance (custodial) | Visa / Mastercard · USD | Varies | Exchange-partnered issuers |

| Lightning-only cards | Lightning node | Lightning BTC | Various · USD | Low merchant support | Various |

The Chimera Card’s differentiation is not in how it settles — card networks are card networks, and settlement happens in USD regardless of wallet. It is in what the wallet does before the card transaction starts: a non-custodial PWA holding user keys, Arkade L2 for low-fee Bitcoin transactions inside the wallet, in-wallet swaps at spreads materially below MetaMask or Phantom, and a non-profit software structure with no incentive to extract value from user flow. When the user chooses to top up the card, the conversion to USDT happens inside the app, and Wirex Pay handles the Visa settlement from there.

For a Bitcoin holder who wants to move BTC cheaply and privately at the wallet level, and who wants the option to spend through a Visa card when needed, that is a meaningfully different architecture from a wallet built around stablecoin spending (MetaMask) or a Solana-denominated cash balance (Phantom). The card is the same at the settlement layer; the wallet beneath it is not.

How to Add Chimera to Your Home Screen

Adding Chimera Wallet to your phone takes under five seconds — no App Store approval, no geographic restriction, no install queue.

Because Chimera is distributed as a PWA, installation is a browser action rather than a store download. The experience on the home screen is indistinguishable from a native app.

On iOS (Safari):

- Open the Chimera Wallet URL in Safari.

- Tap the Share icon at the bottom of the screen.

- Select “Add to Home Screen.”

- Confirm. The icon appears on your home screen and launches like any native app.

On Android (Chrome):

- Open the Chimera Wallet URL in Chrome.

- Tap the three-dot menu in the top right.

- Select “Install app” or “Add to Home Screen.”

- Confirm. The app installs directly to your launcher.

The PWA approach is a deliberate distribution choice — it keeps Chimera accessible even if a store listing is affected by a future platform policy change. The wallet runs in a standalone window with its own icon, indistinguishable from a native app in daily use.

What You Give Up

Chimera is not the right wallet for every user, and pretending otherwise would be dishonest.

Four honest limitations are worth naming:

- Current scope is Bitcoin only. If you hold meaningful positions in Ethereum assets, Solana tokens, or alt-L1s, Chimera’s v0.1 PWA does not serve you today. Multi-asset support is scheduled for end of May 2026, but until that ships, MetaMask, Trust Wallet, or Phantom will continue to be the right tool depending on your chain mix.

- Arkade is new. Mainnet has been live since October 2025, and the backing is strong — Tether, Tim Draper, Anchorage Digital, Ego Death Capital. But Arkade is not Lightning in 2019. It is a newer protocol with a shorter track record, and that is a trade-off users should weigh. Chimera is the first Bitcoin super-app to integrate Arkade as its primary payment layer, which is a credibility signal in its own right, but it does mean you’re using both a new wallet and a new protocol together.

- The card is a top-up model. Once you top up the Chimera Card, funds are converted to USDT in-app and sit on the Wirex Pay rail until you spend. This is true of every crypto card — settlement has to happen somewhere, and on Visa it happens in USD. The architectural difference is where that top-up originates: for the Chimera Card, it originates inside a non-custodial wallet on the user’s device, rather than from a pre-funded custodial balance.

- KYC rules vary by service. Fiat ramp thresholds, card onboarding, and other services each have their own KYC parameters set by the licensed third-party partners that operate them. The Chimera Card requires light KYC through the in-app flow; other services apply their own rules according to their own compliance requirements.

The TGE Window

Chimera’s CEXT token goes to public launch on May 20, 2026, with 90% of the supply going to market — a distribution profile rare in 2026 TGEs and designed to avoid the large insider allocations that have defined recent token launches. Separate editorial coverage of the chimera wallet tge and token launch details the full tokenomics and pre-TGE mechanics for readers who want to go deeper on that side of the product.

For readers who fund a wallet with fiat before the TGE, two mechanics apply. First, the referral program: all verified users earn a percentage of fees from users you refer — 20% base rate, with higher rates available for CEXT holders after TGE. Second, the pre-TGE window itself — funding with fiat before mid-May establishes a position before the public launch.

Referral programs and all other external services accessible through the wallet are independently managed by third-party partners; Chimera as the wallet layer does not collect fees from any of them.

FAQ

Is Chimera Wallet safe?

Chimera Wallet is non-custodial — your private keys are generated and stored on your device, and the wallet only signs transactions. The wallet itself is open-source software developed by a non-profit association that does not hold user funds or operate financial services. The protocol layer is Arkade, which launched on Bitcoin mainnet in October 2025 and is backed by Tether, Tim Draper, Anchorage Digital, and Ego Death Capital. Financial services alongside the wallet — card issuance, token infrastructure, fiat ramps — are delivered by separate licensed partners.

Does Chimera Wallet work without downloading an app?

Yes. Chimera is distributed as a Progressive Web App (PWA) — you access it through your phone’s browser and can add it to your home screen in under five seconds. The PWA is the only distribution channel, so the wallet remains accessible regardless of App Store policy changes.

What is the difference between Chimera Wallet and MetaMask?

The chimera wallet vs metamask comparison is about the wallet layer, not the card. MetaMask is a general-purpose cross-chain wallet — BTC, EVM, Solana, Monad — with the MetaMask Card spending USDC, USDT, and WETH at any Mastercard terminal. Its Bitcoin support is L1-only. Chimera is built on Arkade L2 for low-fee Bitcoin transactions, distributed as a PWA, and developed by a non-profit association rather than a for-profit company. Both cards settle on stablecoin rails (MetaMask via Baanx, Chimera via Wirex Pay) — the difference is in what the wallet does before any card transaction happens. The chimera wallet vs trust wallet comparison is similar: Trust Wallet optimises for chain breadth (100+ chains, no first-party card); Chimera optimises for a non-profit software layer with genuinely decentralised Bitcoin infrastructure underneath.

What is the Chimera Card?

The Chimera Card is a Visa card powered by Wirex Pay, available in 50+ countries across Europe, Asia-Pacific, and Latin America. You top it up from the Chimera Wallet, the top-up is converted to USDT in-app, and the card settles every transaction in USD on the Visa network — the same way every major crypto card works. Pre-orders are live now (1,000 priority cards, 20 CHF reservation), with virtual cards shipping first and physical cards following. Pre-order holders lock in 1.5% transaction fees and 0% top-up fees for the lifetime of the account. Light KYC is required through the in-app flow.

Does Chimera Wallet work in the US?

Yes. The Chimera PWA is accessible globally through a standard web URL, and the licensed third-party partners delivering card, fiat, and token services operate in the US where their own regulatory permissions allow. Fiat services apply light KYC when required by the licensed partner’s compliance requirements.

The Honest Conclusion

MetaMask for DeFi and cross-chain stablecoin spending. Trust Wallet for chain breadth. Phantom for Solana and Solana-backed card spending. Chimera for low-fee Bitcoin transactions at the wallet layer, a non-profit software structure, and a Visa card for spending when you need it.

None of these wallets is universally better than the others — they are built for different users solving different problems. What makes Chimera distinct in April 2026 is not that it solves a gap nobody else is solving — every major wallet now has a spending path. It is that Chimera is the only wallet in this comparison where the software is developed by a non-profit, Bitcoin moves inside the wallet on Arkade L2 rather than L1, and the fee structure is materially lower than the incumbents on the transactions users actually make.

For users who want a non-custodial wallet with low fees, genuinely decentralised Bitcoin infrastructure, and a card for when they need to spend — backed by a software architecture that is not under pressure to extract value from them — Chimera Wallet is worth a look. The PWA is live now with Bitcoin support; multi-asset support and the CEXT token launch ship through May 2026; Arkade P2P swaps follow in June. Readers tracking the token side of the product can also follow the chimera wallet tge and token launch for the May 20 public launch.