Stock: Falls Despite over 20% YoY Performance and $1B Buyback")

TLDR

-

Q1 FY26 revenue rose 20% YoY to $1.10 billion

-

Net new ARR grew by $194 million, total ARR hit $4.44 billion

-

GAAP net loss widened, but non-GAAP income remained solid

-

Announced a $1 billion share repurchase plan

-

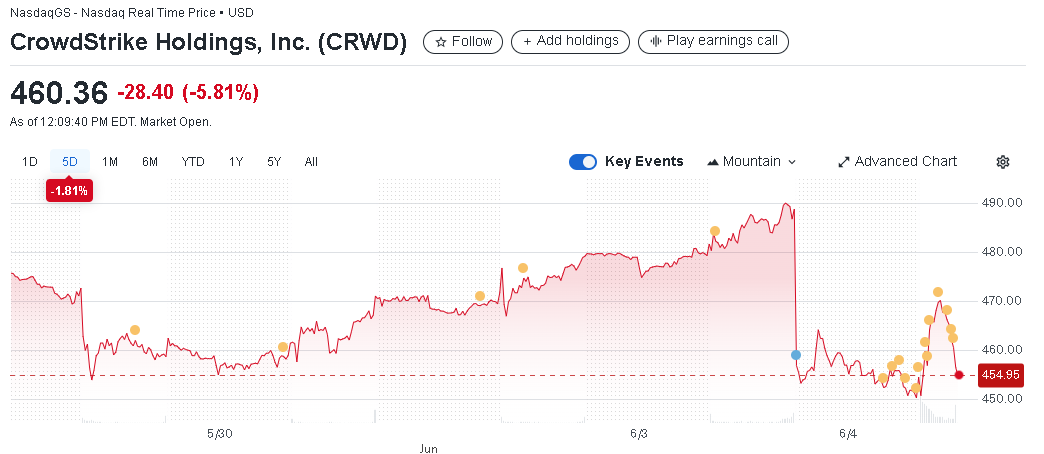

Stock dropped 5.75% to $460.63 despite strong fundamentals

CrowdStrike Holdings Inc. (NASDAQ: CRWD) stock traded at $460.63 as of writing, down 5.75%, following its first-quarter fiscal 2026 results announced on June 3, 2025.

CrowdStrike Holdings, Inc. (CRWD)

Despite delivering a strong performance, the stock declined, possibly on profit-taking after a stellar year-to-date return of 34.62%. The company posted record financial results and reinforced its commitment to growth with a $1 billion share repurchase authorization.

Robust Financial and Operational Metrics

CrowdStrike’s total revenue for Q1 FY26 reached $1.10 billion, up 20% year-over-year. Subscription revenue also rose 20% to $1.05 billion. Annual Recurring Revenue (ARR) climbed 22% to $4.44 billion, including $194 million in net new ARR.

While GAAP loss from operations widened to $124.7 million, non-GAAP income from operations stood at a healthy $201.1 million. GAAP net loss was $110.2 million, compared to last year’s $42.8 million profit. However, non-GAAP net income was $184.7 million, or $0.73 per share.

$CRWD | CrowdStrike is -7.1% after-hours

🔹 EPS: $0.73 vs. $0.66 est. ✅

🔹 Revenue: $1.10B vs. $1.10B est. 🟠Key takeaways:

🔸 Subscription rev: +21% YoY

🔸 ARR: +22% YoY

🔸 Authorized $1B in share buybacks

🔸 FY EPS outlook: $3.50 ($3.39 prior)

🔸 Q2 revenue outlook: ~$1.15B pic.twitter.com/yCYtmwXk1S— CMG Venture Group (@CmgVenture) June 3, 2025

Record Cash Flow and Shareholder Confidence

CrowdStrike achieved record cash flow from operations at $384.1 million and free cash flow of $279.4 million. Cash and equivalents reached $4.61 billion. To underscore its long-term confidence, the board approved a $1 billion share repurchase program, signaling strength and stability.

Falcon Flex and AI-Driven Growth

The Falcon platform, including Falcon Flex, is rapidly gaining market traction. Falcon Flex accounts exceeded $3.2 billion in total deal value, growing over six times year-over-year.

CEO George Kurtz highlighted CrowdStrike’s role in driving cybersecurity for the “agentic AI era.” New offerings like Falcon Privileged Access and Charlotte AI workflows are setting standards in identity protection and AI-driven threat management.

Market Recognition and Strategic Collaborations

The company received several accolades, including Google Cloud’s 2025 Security Partner of the Year. It also expanded its collaboration with Microsoft to improve coordinated threat actor tracking. Falcon innovations now span cloud, endpoint, SaaS, and exposure management, helping organizations replace legacy tools and enhance cyber resilience.

Financial Outlook Supports Growth Trajectory

While GAAP profitability remains a challenge, CrowdStrike reaffirmed its strong net new ARR pipeline and margin expansion goals for the second half of FY26. Module adoption continues to rise, with 22% of customers using eight or more Falcon modules.

Conclusion

Despite the dip in stock price, CrowdStrike’s Q1 results demonstrate robust growth and operational excellence. Its continued investment in AI, innovation, and strategic partnerships positions it as a leader in cybersecurity as it aims for $10 billion in ARR.

Stop guessing and start investing with confidence. KnockoutStocks gives you the AI insights, market intelligence, and stock research you need to spot opportunities, cut through the noise, and make smarter investment decisions — all in one powerful platform.

Sign up today and get 50% OFF full access to our premium stock picks.

Simply use coupon code SPECIAL50 at checkout to claim your exclusive discount.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants