TLDR

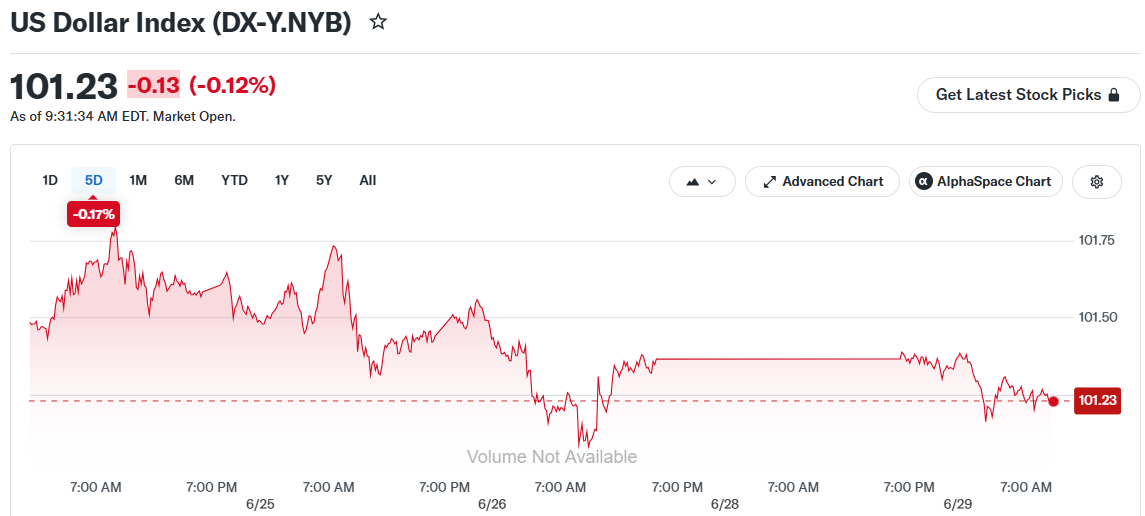

- The U.S. Dollar Index slipped to 101.24 but remains near a 14-month high

- The dollar is on track for its biggest monthly gain since July 2025, up roughly 2.5% in June

- U.S.-Iran peace talks are resuming in Qatar, easing some safe-haven demand

- Fed is expected to raise rates twice more by December, with inflation above 4%

- ECB’s Sintra Forum and U.S. jobs data are the key events to watch this week

The dollar pulled back slightly on Monday but stayed close to a 14-month high. The U.S. Dollar Index was at 101.24 during early U.S. market hours, down from a peak of 101.8 hit on June 24.

Despite the small dip, the dollar is still heading for its strongest monthly performance since July 2025. The index is up around 2.5% in June alone.

What’s Driving Dollar Strength

Several factors have kept the dollar elevated. Inflation in the U.S. is running above 4%, pushing the Federal Reserve toward a more aggressive rate stance. Markets are now pricing in two more 25-basis-point rate hikes before the end of the year.

Strong U.S. economic data has added to that picture. A resilient labor market has kept investor confidence in the dollar high, and this week’s non-farm payrolls report will be closely watched for any signs of change.

Capital flows into U.S. artificial intelligence stocks have also played a role. Global investors moving money into Wall Street have kept underlying demand for dollar-denominated assets steady.

Geopolitics and Global Central Banks

The U.S.-Iran conflict was a key driver of dollar safe-haven demand in recent weeks. The two countries exchanged attacks over the weekend before agreeing to halt further military action. Peace talks are set to resume in Qatar on Tuesday.

The ceasefire has started to ease some of the pressure in global energy markets. Crude oil prices have begun pulling back toward pre-conflict levels as tanker flows from the Persian Gulf pick up following a memorandum of understanding between Washington and Tehran.

The euro edged up 0.2% to $1.14 but remains near a one-year low. The British pound held steady at $1.32 as attention shifted to a major political transition. Former Prime Minister Keir Starmer resigned last week, and Andy Burnham is seen as the frontrunner to succeed him.

The ECB’s annual Sintra Forum opens Monday. ECB President Christine Lagarde will deliver opening remarks alongside Fed Chair Kevin Warsh and Bank of England Governor Andrew Bailey. Markets expect at least one more ECB rate hike this year after the deposit rate was raised to 2.25%.

The Japanese yen was flat. Japan’s Bank of Japan Tankan survey is due this week and is expected to show improved business sentiment despite recent energy disruptions.

Across Asia, traders are also watching China’s manufacturing data, South Korea’s trade figures, and India’s industrial production numbers for clues on regional monetary policy direction.

The dollar’s path this week will largely depend on what central bank officials say at Sintra and what Friday’s jobs report shows.

Stop guessing and start investing with confidence. KnockoutStocks gives you the AI insights, market intelligence, and stock research you need to spot opportunities, cut through the noise, and make smarter investment decisions — all in one powerful platform.

Sign up today and get 50% OFF full access to our premium stock picks.

Simply use coupon code SPECIAL50 at checkout to claim your exclusive discount.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants