TLDR

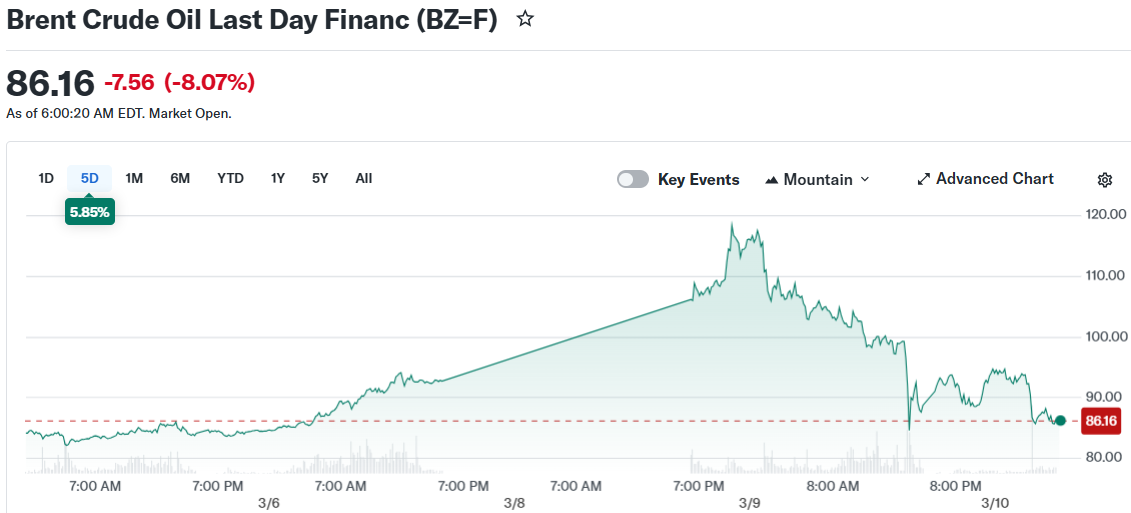

- Brent crude fell 6–7% to around $92 on Tuesday after hitting highs above $119 on Monday

- Trump said the war against Iran was “very complete” and ahead of his 4–5 week timeline

- Iran’s IRGC rejected that framing and threatened to block all regional oil exports

- G7 nations said they were ready to release emergency oil reserves but held off

- Goldman Sachs kept its Brent forecast at $66/barrel for Q4 2026, citing a fluid situation

Oil prices swung wildly this week as conflicting signals from the U.S. and Iran kept energy markets on edge. Brent crude dropped roughly 7% on Tuesday to around $92 a barrel, just one day after surging past $100 for the first time since mid-2022.

The sharp rise Monday was driven by supply fears. Saudi Arabia and other producers had cut output as the U.S.-Israeli war on Iran expanded, pushing Brent as high as $119.50 and West Texas Intermediate to $119.48. That marked the largest single-day intraday swing on record, according to Dow Jones Market Data.

The reversal came after Trump told CBS News on Monday that the war was “very complete” and that the U.S. was “very far ahead” of his initial four-to-five week timeline. That comment alone calmed markets and triggered a selloff in oil.

Russian President Vladimir Putin also spoke with Trump on Monday, sharing proposals for a quick settlement. That added to the de-escalation mood and accelerated the price drop.

But not everyone was ready to call the conflict over.

Iran Pushes Back

Iran’s Islamic Revolutionary Guard Corps said Tuesday that they, not the U.S., would “determine the end of the war.” The IRGC also threatened to block all oil exports from the region if U.S. and Israeli strikes continued.

Iran’s Foreign Minister Abbas Araghchi separately ruled out any talks with the United States in an interview with PBS News, as reported by the Wall Street Journal.

🇺🇸🇮🇷🇨🇳 Trump threatens to hit Iran "TWENTY TIMES HARDER" if they disrupt oil in the Strait of Hormuz, then calls the entire operation "a gift from the United States to China."

Keeping the Strait open was always the real objective.

And now he's leveraging it as a bargaining chip… https://t.co/eyhWHSlL2G pic.twitter.com/4BgTk5ar3E

— Mario Nawfal (@MarioNawfal) March 10, 2026

Trump responded directly on Truth Social, warning Iran that any move to block the Strait of Hormuz would result in the U.S. hitting Iran “twenty times harder than they have been hit thus far.”

Analysts noted the market may be getting ahead of itself. “While there was an overreaction to the upside yesterday, we think there is an overreaction to the downside today,” said Suvro Sarkar, energy sector team lead at DBS Bank.

He pointed out that Murban and Dubai oil grades were still trading above $100 a barrel, suggesting physical supply conditions had not changed much on the ground.

What Governments Are Doing

The G7 finance ministers met Monday to discuss releasing emergency oil reserves. They stopped short of doing so, but issued a statement saying they “stand ready to take necessary measures,” including a stockpile release.

Trump is also reportedly considering easing oil sanctions on Russia as part of a broader effort to cool prices. Multiple sources confirmed the option is on the table.

Analyst Priyanka Sachdeva of Phillip Nova said the combination of those signals — possible Russian sanctions relief, G7 reserve releases, and Trump’s comments — gave traders enough reason to back off the panic buying.

Goldman Sachs said it was not changing its oil price forecast. The bank still expects Brent at $66 per barrel and WTI at $62 per barrel for the fourth quarter of 2026, citing the fluid nature of the situation.

Iran’s IRGC statement on Tuesday remains the most recent hard signal that the conflict is not winding down.

Stop guessing and start investing with confidence. KnockoutStocks gives you the AI insights, market intelligence, and stock research you need to spot opportunities, cut through the noise, and make smarter investment decisions — all in one powerful platform.

Sign up today and get 50% OFF full access to our premium stock picks.

Simply use coupon code SPECIAL50 at checkout to claim your exclusive discount.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants