It’s simple to be an armchair investor. Just pull up a chart of the latest hot crypto, stock, or ETF and bewail the fact that you didn’t have all of your life savings riding it to insane new highs. Most, if not all, crypto traders have experienced similar remorse at one time or another. Looking closer, however, there are many sound reasons to never plow the majority of your risk capital into any single crypto. Some of the rationales are obvious, but others will require you to think outside of the box. Limiting portfolio overconcentration is easy enough, as long as you keep your emotions, fear of missing out (FOMO), and greed in check. Here’s a closer look now.

A Fraction of Your Net Worth

In this article, we’re looking at how to avoid investing too much of your risk capital into any given trade. We won’t be discussing the equally important issue of how much of your net worth should be allocated for crypto investing and speculation. However, let’s just say that you should strive to allocate only a fraction of your total net worth (house, personal property, savings, retirement accounts, etc.) into the crypto markets. Only you can determine the appropriate amount to invest in cryptos. However, it should be modest enough so that if you were unfortunate enough to lose it all, your lifestyle would not be affected.

Divide Your Portion Unto Seven or Eight

King Solomon’s timeless commentary is perhaps the best portfolio diversification advice you’ll ever receive:

“Divide your portion to seven, or even to eight, for you do not know what misfortune may occur on the earth.”

- Ecclesiastes, chapter 11, verse 2

The fatal mistake that many crypto investors make is putting a huge amount of their risk capital into one trade or long-term position. You may also have succumbed to this temptation. Perhaps you were lucky and you made a bundle, or maybe you lost big-time.

Maybe you even followed Solomon’s advice, dividing all of your risk capital across seven or eight different coins. Then came the December 2017 crypto blow-off top, and you still got whacked with 80 percent account drawdowns. What gives, anyway?

Well, for one thing, Solomon wasn’t saying put all of your risk capital into equal allocations of crypto. Most crypto markets are highly correlated, so you’re really not diversifying very much at all.

Solomon was referring to allocating your risk capital across significantly different kinds of investments. In previous articles, you’ve seen the relative strength performances of Bitcoin vs. tech stocks, gold, real estate, and emerging markets stocks. Bitcoin was the unchallenged winner over the past two-, three- and five-year periods. However, Bitcoin has severely underperformed all four of those financial asset classes since December 2017. King Solomon might have suggested that you allocate an equal dollar amount of your risk capital across all five of those key markets. You would have enjoyed a smoother portfolio equity curve, simply by limiting portfolio overconcentration.

[thrive_leads id=’5219′]

The Fatal Deception

Bitcoin declined by nearly 85 percent between December 2017 and December 2018, making a powerful case for conservative asset allocations. Such a decline would have been dismissed as unlikely (if not impossible) by many late-stage (Q4 2017) Bitcoin investors. Consequently, they may have plowed far too much cash into the coin as it soared ever higher. Then when Bitcoin reversed hard to the downside, they might’ve experienced extreme stress, if not outright panic.

Traders and investors often forget that the outcome of any given trade is almost 100 percent random. The outcome is independent of all the series of winners (losers) that preceded it. And yet, crypto enthusiasts can still be tempted to bet the ranch based on favorable news, chart patterns, or extremes in investor sentiment. Should any rational investor deploy two-, five- or even 10 times their normal cash allocation on a trade that’s really just a 50-50 tossup? Of course not. Yet, traders and investors continue to make this critical mistake every single day.

One way investors can avoid this trap is to simply follow Solomon’s wise counsel.

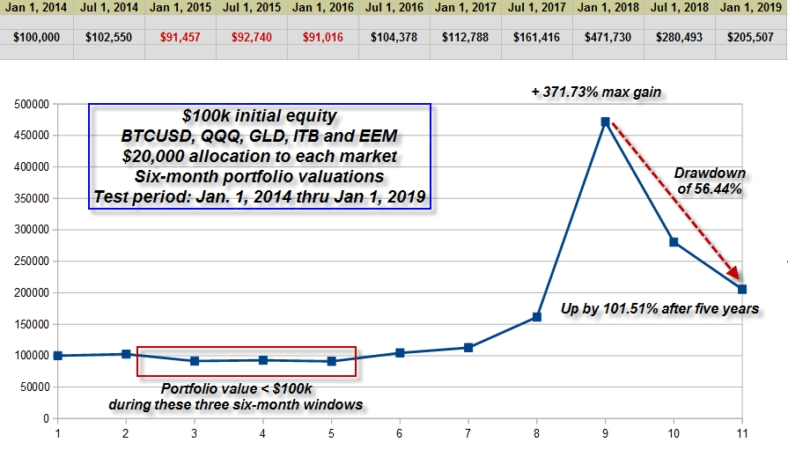

Diversity: Bitcoin Plus ETF Allocations

Here are the key stats for a hypothetical, $100,000 portfolio containing Bitcoin, QQQ (NASDAQ 100 ETF), GLD (gold ETF), ITB (real estate ETF), and EEM (emerging markets ETF). To recap from our previous articles The test period was January 1, 2014, through January 1, 2019, measured at 6-month intervals. $20,000 was allocated to each of the five instruments:

The above Bitcoin plus four ETF portfolio was profitable. The portfolio never dropped below $91,000 during a nearly 18-month long initial drawdown. However, after running up by nearly 400%, it gave back more than $265,000 on open gains. Bitcoin was the asset most responsible for the severity of each drawdown in portfolios one and two.

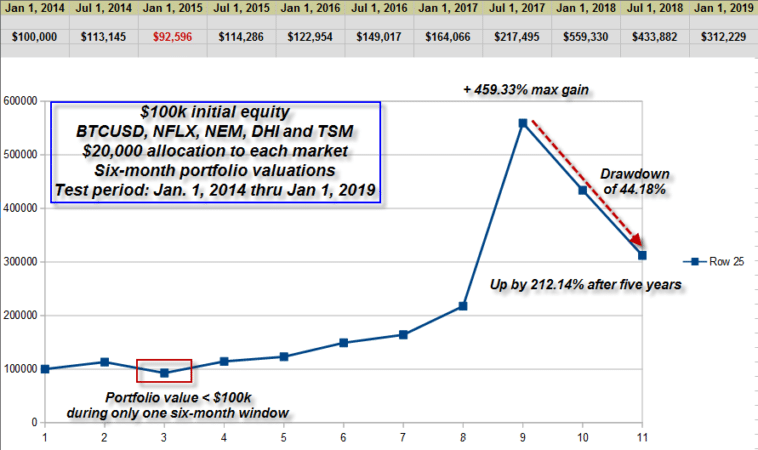

Diversity: Bitcoin Plus High-Beta Stock Allocations

This next portfolio incarnation substituted the portfolio one ETFs with one of its high-beta (volatile) stock components. Performance increased substantially, even as drawdowns lessened considerably. This portfolio offered the best mix of profit potential, low drawdown (particularly underwater drawdown) and risk control.

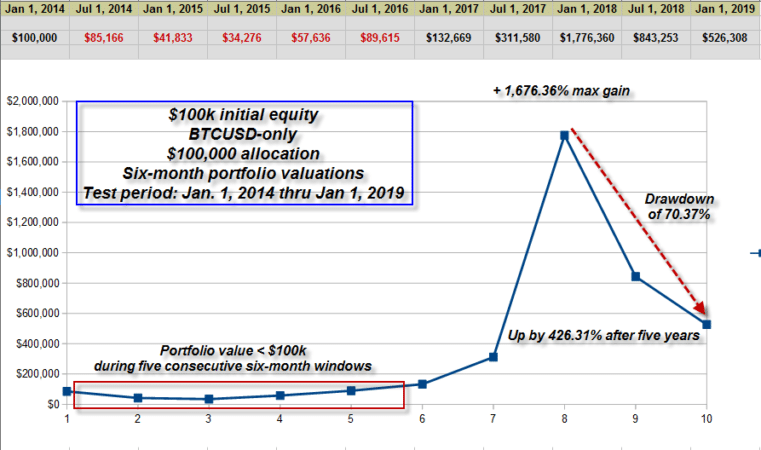

The Wild Ride: Bitcoin Alone

The Bitcoin-only portfolio produced amazing gains. However, those gains came with a heavy price tag, such as a huge, open-profit drawdown. Would you really have been able to stomach a $65,000 underwater drawdown 18 months after (July 1, 2015) making your initial $100,000 Bitcoin investment?

Okay, Monty. I’ll Take Door Number Two

Realistically, portfolio two would have been the one to run with. Here’s why:

- The high-beta ETF component stocks offered way more profit potential than the ETFs did.

- The stocks actually made the portfolio more risk-averse with smaller duration, less severe drawdowns.

- The high-beta stocks appear to complement Bitcoin nicely, being a volatile market itself.

The Bitcoin-only portfolio offered the most profit potential. By far, no debate at all. However, it also would have been the most difficult for investors to stay with for the long haul. Very few investors (crypto or otherwise) can handle 70-percent open-gain drawdowns. Nor can many deal with the stress of a nearly 65-percent underwater equity drawdown (when your portfolio drops beneath its original value), and that’s right out of the gate! Neither portfolio one or two had drawdowns even remotely as severe as did the Bitcoin-only portfolio. All told, portfolio two looks to be the hands-down winner in this three-way shootout.

Limiting Portfolio Overconcentration

You’ve seen how limiting portfolio overconcentration can limit drawdown duration and intensity, even while enhancing profitability. There’s no perfect way to design a balanced investment portfolio, and surely the above models can be tweaked, retested and improved upon.

However, the big idea is that you understand the importance of diversifying across fundamentally different asset classes (at least five and perhaps as many as ten) in equal dollar amounts. As you become skilled in doing so, your portfolio equity curve will become straighter. Your drawdowns will be smaller and your stress level will also diminish.

Here’s a memorable quote that sums up at least some of what you’ve learned above:

“I am more concerned with the return of my money than the return on my money.”

- Will Rogers